Diversification – Controllable and Uncontrollable Risks

One of the major differences between quant systems and traditional equity-based funds is in the area of risks.

With quant systems, the architect can design the system to achieve a minimum acceptable risk. With traditional equity-based funds, the risk is uncontrollable.

Let us understand this in a bit more detail. When considering the risks associated with stock market (equity-based) investments, we need to be aware of the following facts:

- The risk of shares in the stock market consists of two components, market risk and company-specific risk.

- Company-specific risks can be eliminated by holding a diversified portfolio of stocks.

- Company-specific risks account for approximately half of the total risk of a portfolio of stocks.

- Market risks in a portfolio of stocks cannot be eliminated.

- That part of the risk a stock which can be eliminated is called diversifiable (or company-specific) risk; that part which cannot be eliminated is called non-diversifiable (or market) risk.

Investors in equity-based investment portfolios / funds therefore have to live with the fact that the market risks cannot be eliminated.

However, the market risks in a stock / share portfolio can be minimised (reduced) by diversifying into other investment asset classes. A balanced investment portfolio would therefore consist of a portfolio of stocks, and it would include other investment asset classes such as fixed-interest investments, property and others.

The challenge is to find other investment asset classes that will improve the balance of the investment portfolio and reduce its overall risk.

The Quant Fund is a new investment asset class that would compliment any balanced investment portfolio. Each balanced investment portfolio should have some investment into the investment asset class

provided by the Quant Fund — which has a “High Return, Low Risk” profile.

A Discussion on Investment Liquidity

A definition of liquidity is as follows:

“Liquidity refers to the efficiency or ease with which an asset or security can be converted into ready cash without affecting its market price”.

The most liquid asset of all is cash itself. Let us explore this definition from an investor's perspective.

If an investor needs to convert an asset or security into cash, he/she would like to do it without incurring a loss. So, if the value of an asset or security is currently less than its original capital, the investor is unlikely to use that particular asset or security to convert into cash.

So, while it might be possible to convert an asset or security into ready cash without affecting its market price, in practice, the investor will consider this asset or security to be illiquid, because the investor will not touch this asset or security until its value exceeds the value of its original capital.

From an investor perspective, the definition should be changed to read as follows:

“Liquidity refers to the efficiency or ease with which an asset or security can be converted into ready cash without affecting its market price and when the asset or security is in positive territory”.

With this new definition of liquidity;

- Most equity investments / funds will typically be “illiquid” for long periods of time within the first several years of an investment.

- Most property investments will also typically be “illiquid” for long periods of time within the first several years of an investment.

By contrast, the Quant Fund is highly liquid from the first month of investment.

The Myth of the Risk-Free Rate of Return

The risk-free rate of return is the theoretical rate of return of an investment with zero risk. The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time.

The so-called "real" risk-free rate can be calculated by subtracting the current inflation rate from the yield of the Treasury bond matching your investment duration. Herein lies the problem. Very often, when calculating the “real” risk-free rate, it will be negative

because the rate of inflation is higher than the treasury bond interest rate. So, in practice, the “real” risk-free rate of return does not exist.

If an investor relies upon cash, fixed-interest investments and bonds, there is a high probability that, at times, the investment portfolio will be losing value in real terms because the rate of inflation is higher than the returns on these investments.

This reality forces investors out of the comfort zone of the illusion of a risk-free environment

(because it does not exist) to consider strategies on how to beat inflation safely.

To date, the majority of investors have considered Equities and Property, both of which have risk profiles that are “Average Return, High Risk”.

Now investors have a new investment asset class to consider. The Quant Fund is a new investment asset class that offers investors a risk profile that is “High Return, Low Risk”. The Quant Fund offers investment portfolios a low-risk method of diversification and beating

inflation, thereby avoiding the relatively high risks of the stock market.

The Myth of Investment Diversification

As a principle, it is a sound strategy for any investment portfolio to be diversified in terms of different investment asset classes. The purpose of investment diversification is to reduce the overall risk of an investment portfolio.

However, the majority of investment funds are restricted to only three high-level asset classes, namely:

- - Cash / Fixed Interest Investments / Bonds —Low Returns, Low Risk.

- Equities or Equity-Based Funds —Average Returns, High Risk.

- Property — Average Returns, High Risk.

And since the risk profile of Equities and Property is similar, the majority of investors, really only have two risk profiles to consider, namely:

- Low Return, Low Risk (Cash, Fixed Interest, Bonds).

- Average Returns, High Risk (Equities and Property).

Some advisors will recommend investors diversify by splitting their funds across different types of funds (eg. Conservative / Large Cap “Blue Chip”, Mid Cap, High Growth Small Cap funds, etc.). However, this form of diversification does not change the risk profile of the investment portfolio because they

are all part of the same investment asset class. They all have a similar risk profile. When the stock market falls, the entire market falls.

What investors need to achieve genuine diversification of their investment portfolios and to genuinely reduce the risk of their investment portfolios is a new investment asset class. An investment asset class that is different from the two they already have.

It would also be ideal if this new investment asset class had a risk profile that was high returns and low risk.

The Quant Fund has been designed to achieve exactly this objective. To be a fund that generates high returns at a very low risk. Proof that this has been achieved is that the Quant Fund has a very high Sharpe ratio. For more information on the Sharpe ratio, click HERE.

The Quant Fund establishes a new investment asset class that will help all investment portfolios to reduce their risks (and improve returns). The Quant Fund should therefore be an essential part of the mix of an investment portfolio.

The Sharpe Ratio - How to Compare Investments / Funds?

Most financial planners would agree that performance is not the only consideration for an investor to consider when selecting an investment / fund, and that one has to also consider the riskiness of an investment / fund.

Since risk and return are the primary measures of any investment, we must quantify these measures so that there is a method by which the quality of any investment can be measured.

Fortunately, mathematicians have devised such a tool. In particular, mathematician / economist William F. Sharpe proposed the Sharpe ratio in 1966 as a tool for comparing investments against each other. William F. Sharpe developed this tool as part of his work on developing the Capital Asset Pricing Model (CAPM) for which he eventually won a Nobel prize in 1990.

Since the Sharpe ratio was introduced, there have been several variations proposed such as the Sortino ratio and the Treynor ratio, but the Sharpe ratio remains the most popular measure and the most widely used.

The Sharpe ratio is a single number that takes into account both the performance and the risk of an investment / fund. So, it can be considered as a measure of the quality of an investment / fund. The Sharpe ratio compares the return of an investment with its risk (volatility of returns). Risk is measured as the standard deviation of the returns or the variability of the returns.

The Sharpe ratio is best understood visually. Please see HERE for visual representations.

The Man Who Solved the Market

How Jim Simons Launched the Quant Revolution

By: Gregory Zuckerman

Publisher: Penguin Business, 2019

This is a book about Jim Simons, who was a pioneer in algorithmic trading in New York, and who significantly outperformed Warren Buffet, George Soros, Peter Lynch, etc. Jim Simons founded Renaissance Technologies, a company dedicated to developing trading algorithms and using these algorithms to manage several funds. Renaissance’s Medallion fund has generated average annual

returns of 66% since 1988. At the time this book was published in 2018, the size of the Medallion fund was estimated at some $10 billion.

This book describes the challenges Jim Simons endured in establishing the fund and most importantly it demonstrates that algorithmic trading can generate above-average returns over a long period of time in a reliable, consistent and predictable manner.

The Quant Fund has a lot in common with the Medallion fund in that the approaches, the logic and the rationale to trading are all very similar. The book largely confirms that all of the decisions and the approaches made in the design and development of the system were sound and we were on the right path.

The Quant Fund is the Australian version of the Medallion fund. This book will give any investor very good insights into the world of algorithmic trading (or quant trading) and will help the investor understand how the above-average returns are generated.

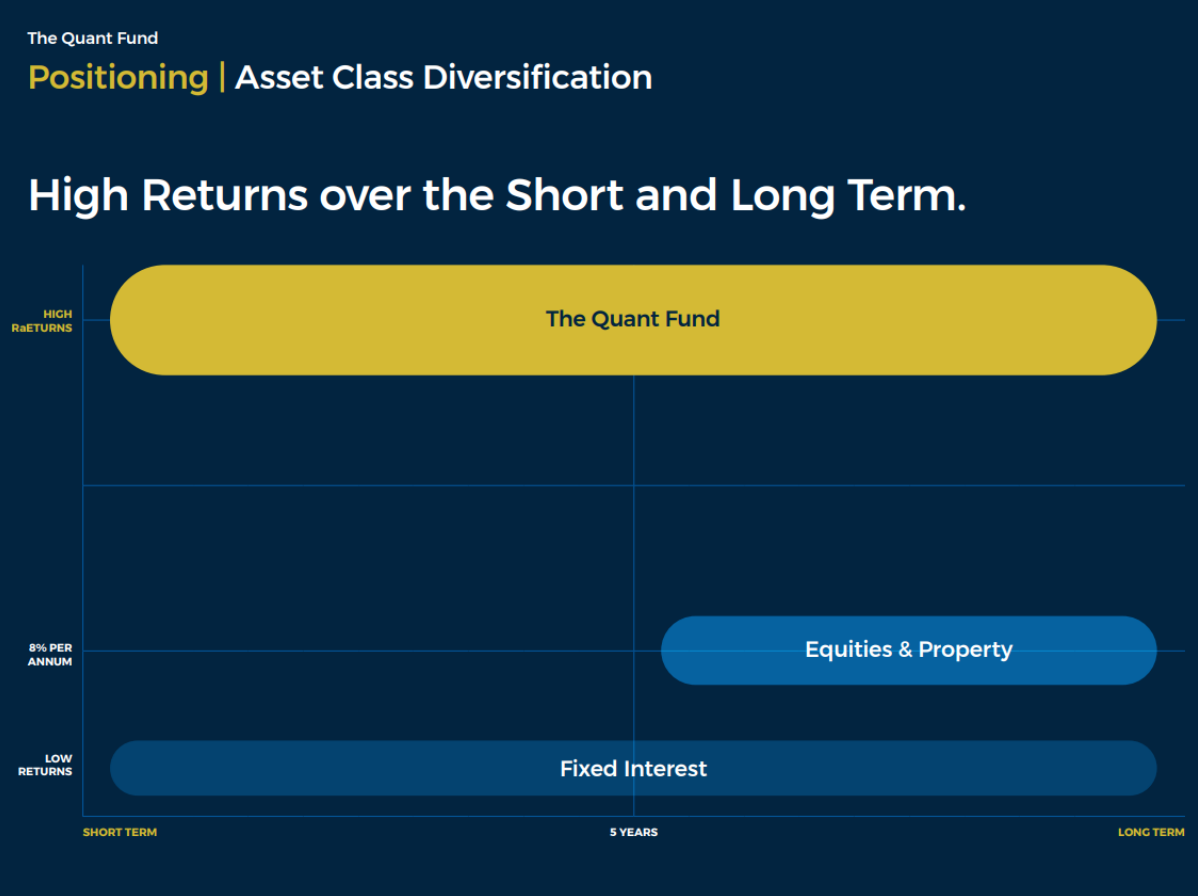

Discussion on Investment Asset Classes

The major investment asset classes include:

- Cash, fixed interest investments, bonds: This class of investment can be both short-term in nature and long-term. With some fixed interest investment, there is a “lock-in” period, typically 1, 2 or 3 years.

- Equities or equity-based funds: This class of investment is a long-term investment as it is only after a period of 5 to 6 years that one can be sure that the value of the investment will exceed its original capital. Equities might perform well in the short term but because of market risk and market volatility, this is not guaranteed. The average long-term performance of this asset class is approximately 8% per annum, with some variance on either side of this number.

- Property: This class of investment is a long-term investment. The average long-term performance of this asset class is approximately 8% per annum, with some variance on either side of this number.

- The Quant Fund is a new investment asset class: This class of investment is both a short-term investment as well as a long-term investment. The performance of this asset class is 20% + per annum.

The slide on the next page positions the major asset class on a grid with expected returns on the vertical axis and investment duration on the horizontal axis. The slide helps to position the salient features of the major investment asset classes and it helps to explain the positioning of the Quant Fund with respect to the major investment asset classes.

The slide also demonstrates that the area occupied by the Quant Fund is not occupied by any other major investment asset class. In fact, the slide highlights the significant gap between the Quant Fund and other investment asset classes.

A balanced investment portfolio should have some interest in all major investment asset classes, including the Quant Fund.

Investment Enquiries

Phone :

1300 900 214

International :

+61 8 6223 0228

Email:

enquiries@thequantfund.com.au